I have to say it, I’ve seen enough.

There has to be something going on in vertical-focused startups that’s boosting their success. (For the uninitiated, these are startups targeting one industry or niche within an industry.)

But before you raise that eyebrow, muscled with doubt, the answer is no.

I don’t have any supporting data, but I’ve been following Greg Head’s Practical Founders community—a hub of bootstrapped companies and those avoiding large VC funding. The stories there, of vertical software companies growing fast with meagre resources (and getting acquired) are compelling and are what make me slow down every time I see one.

So when I saw a vertical fintech company that’s raised $18 million in funding, Constrafor, I had to dig in to see where those dollars are going. If the bootstrapped folks are flourishing, what about their VC-funded counterparts? And how much more can we learn from it…

The big question I had was: what is the right way to “build” a product for a vertical industry? What problems are they addressing and what’s its impact? How is the product packaged and accessed by customers (Place)? What are the pricing models?

Note: Since I’m investigating marketing through the lens of vertical software. I’ll concentrate on the product and how it’s shaped to go to market. Read this from the perspective of a founder thinking through launching a vertical fintech, not a marketer.

Product

In a nutshell, Constrafor is a suite of construction tech software used to manage the activities between contractors and their subcontractors. Right until, it turns into a fintech.

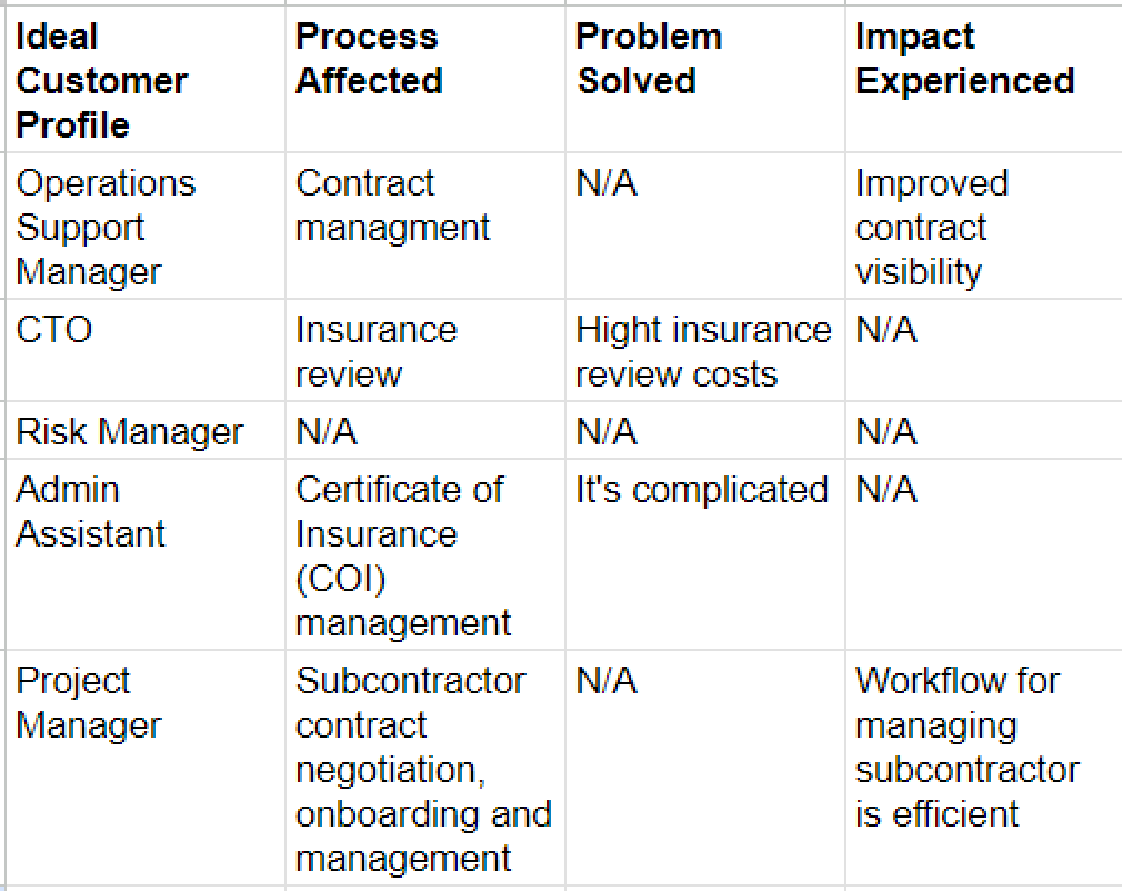

From repeated snooping, I’ve learnt that to figure out what a company’s product really does, don’t look at the product, look at the person the product was designed for.

They’ll lead you to the process the product improves, the problem it solves, the impact and finally, what the product really does for them.

So I started with Constrafor’s customers.

For instance, they help (buyer persona) construction project managers with activities (process Constrafor affects) around subcontractor negotiation, onboarding and management, leading to (impact) an efficient subcontractor management experience.

Use this framework, when analysing the table below.

Now that we have context on the person they market to. Constrafor’s products in the screenshot below should make much more sense.

Constrafor is simply a product for automating back office tasks, but niched down to general contractors and subcontractors. The key process this product affects is procurement; with the following sub-processes within:

- Managing contracts between the general contractor, clients and subcontractors

- Payment processing: general contractors have to send money to their subcontractors, this can be manual and time consuming

- Insurance compliance: every general contractor has to get a certificate of insurance (COI) as proof of compliance.

- Prequalification: Constrafor’s ideal customer profile (ICP) works with subcontractors to deliver projects and needs to assess their capabilities through a prequalification process that involves lots of data collection.

- Invoice management: the general contractor receives multiple invoices from different subcontractors that they have to approve and monitor to know which ones are still pending payment.

- Diversity procurement: involves verifying that subcontractors have diversity certificates, especially when working on projects that have quotas around diversity.

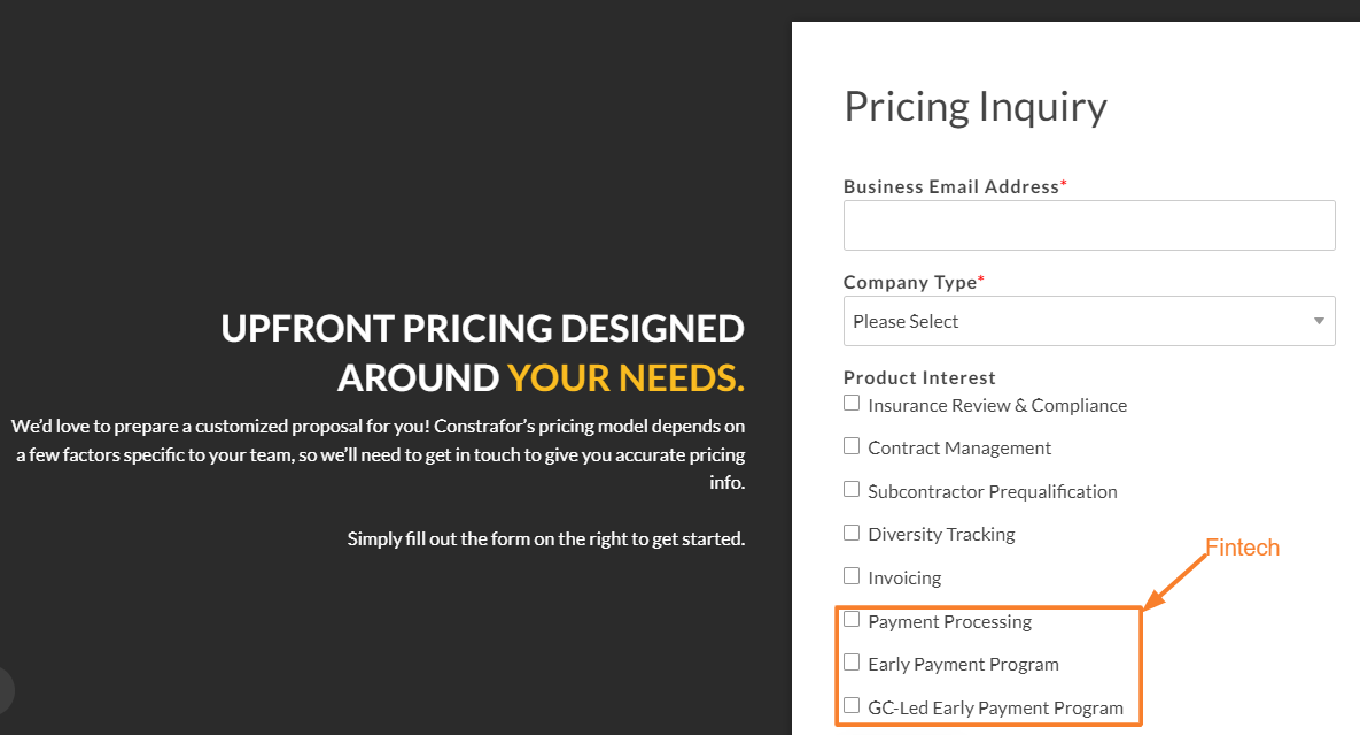

How embedded finance comes in

Constrafor has built software for all these processes, but the fintech bit comes at the payment processing stage where they offer to automate payments in place of issuing and shipping checks—a process that’s still pervasive in the construction industry.

The company has also embedded loans as a product: to allow contractors to pay their subcontractors early without having to pay extra. More about this in the “Price” section.

Throughout my snooping, I kept wondering, “what are they really? A fintech?” They don’t really look/brand themselves like the hardcore fintechs I’m used to, but they do smell like them.

They’re probably a peek into the future, a world where every company could be a fintech.

My best bet is, Constrafor achieved this by looking at all the processes around the relationship between general contractors and subcontractors, built software for them, then included fintech.

But this order seems to be changing. At first glance, I thought fintech was secondary to its main value proposition but I was wrong.

At the time of writing this, I found that the company is hiring a growth marketer and the job description spilled the beans. The new person is specifically coming in to promote and expand the adoption of their early-pay loan product.

Why is fintech valuable for a vertical like construction?

For starters, we’re dealing with large construction project payments here. That’s a high transaction value revenue potential opportunity if more contractors use it.

Also, consider this, 74% of Shopify’s $ 7.1 billion, 2023 revenue came from its financial services operations. Constrafor might be seeing what Shopify saw: more potential on the financial side of the construction vertical it serves than the operational software side. Only time will tell.

Another thing to keep in mind is, in what verticals will the revenue from a pure fintech product be enough to sustain a company without having to create multiple software products as Constrafor has done?

Is it possible to grow a one-product vertical fintech? (Cause every vertical fintech company I’ve looked at has had to build and bundle multiple products. Why?)

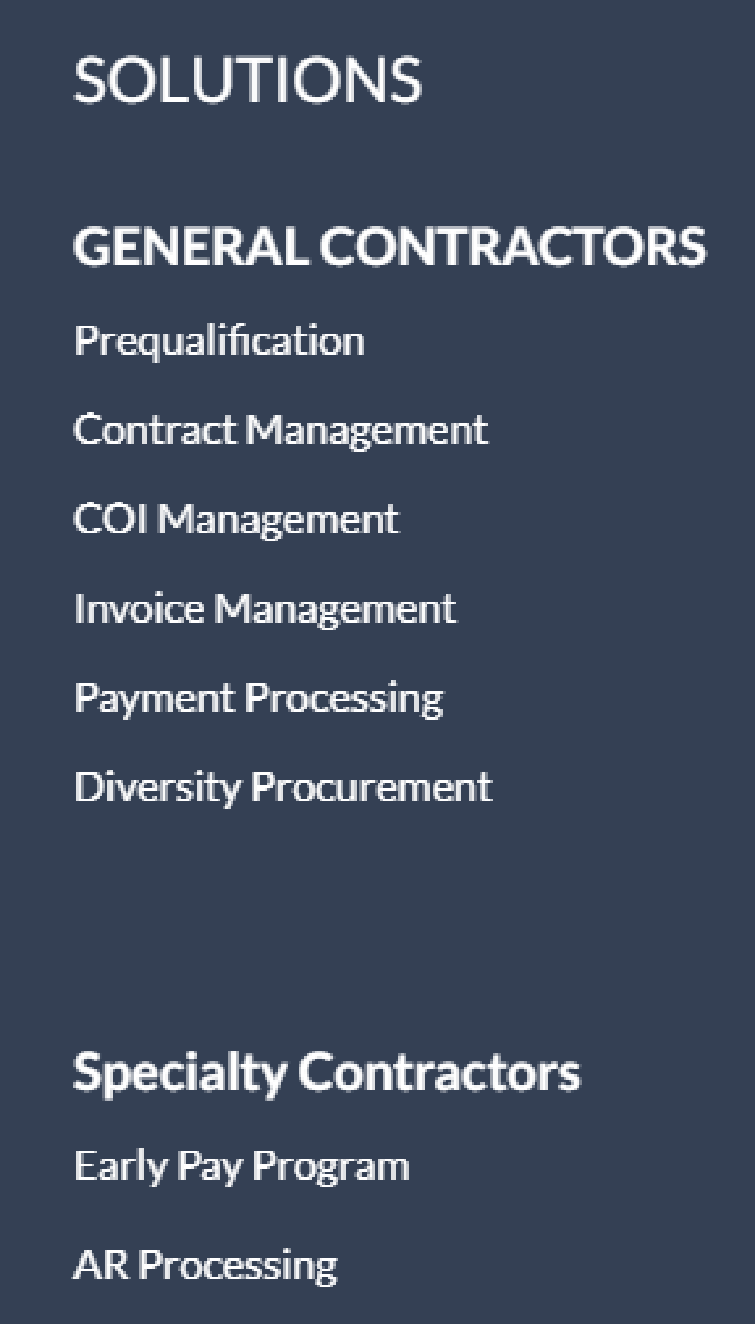

Price: The world of bundles

Since this company is serving one industry, it limits the number of companies in its total addressable market compared to serving everyone.

But the beauty of vertical software companies is that because they are tailored for one ICP, these companies can bundle multiple products; creating room for expansion and upsells.

Constrafor has 8 products in its portfolio, as shown in the screenshot below.

This way, Constrafor can get its hands into a company’s pockets through a small, low-cost solution; opening up 7 other different products they can use as market entry points.

Another pricing decision to note is how Constrafor has divided its early-pay product into two, based on who’s paying the cost of the loan.

If the subcontractor requests early pay, they only need to get an approved invoice from their general contractor and they get the loan without their contractor knowing. But if the request comes from the general contractor, they are the ones to bear the cost.

This model has the potential to introduce marketing virality from both parties: with both general contractors and subcontractors capable of influencing their partners to use Constrafor to access these features.

This is epitomised in a testimonial from a subcontractor using the early-pay product, describing how they can take on projects with long payment terms and how they “wouldn’t take on these projects without it [early-pay].”

Connecting these dots to what I’ve seen in the B2B Buy Now Pay Later (BNPL) space (look at what Playter or Crossflow is doing), the ability to shift the “who pays?” decision, is allowing startups to attack traditional trade finance markets from multiple angles.

One day, their ideal customer profile (ICP) could be the companies paying the invoices, the next it’s the company getting paid. Constrafor is serving both sides.

All in all, from the experience of a fintech nerd digging through Constrafor’s customers and products, I’d say to whoever is curious about building a fintech product for a vertical niche, if you just start by looking at the processes within that industry, your fintech eyes will eventually land somewhere financial.

Okay, before I fall down another rabbit hole, let’s leave it there. Off to drink some Kenyan tea, see you on the next one…